Featured

Table of Contents

- – Assessing Home Equity Options in Fargo North D...

- – The Mathematics of Interest Reduction in the ...

- – Picking Between HELOCs and Home Equity Loans

- – The Risk of Collateralized Financial Obligation

- – Nonprofit Credit Therapy as a Safeguard

- – Tax Implications in 2026

- – The Step-by-Step Debt Consolidation Process

Assessing Home Equity Options in Fargo North Dakota

House owners in 2026 face an unique financial environment compared to the start of the decade. While home values in Fargo North Dakota have stayed fairly stable, the expense of unsecured consumer debt has climbed significantly. Charge card rates of interest and individual loan expenses have actually reached levels that make carrying a balance month-to-month a major drain on family wealth. For those residing in the surrounding region, the equity built up in a main home represents among the few staying tools for lowering total interest payments. Utilizing a home as collateral to pay off high-interest debt needs a calculated technique, as the stakes involve the roofing system over one's head.

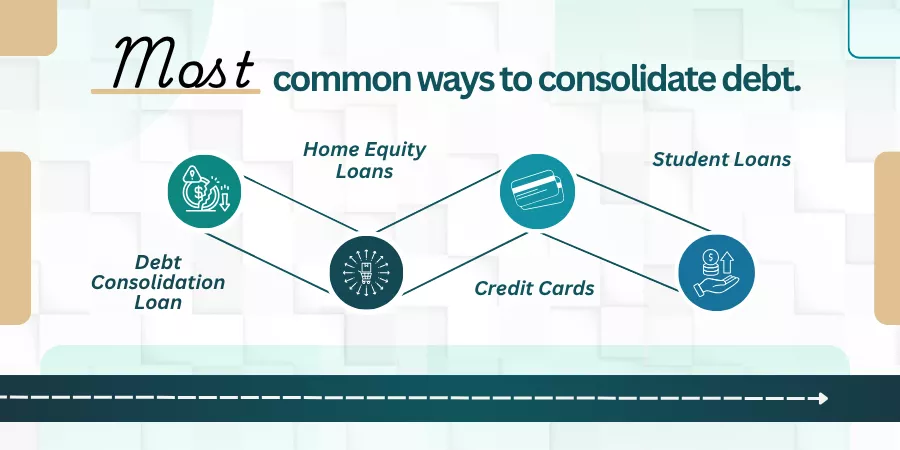

Rate of interest on credit cards in 2026 typically hover between 22 percent and 28 percent. A Home Equity Line of Credit (HELOC) or a fixed-rate home equity loan usually brings an interest rate in the high single digits or low double digits. The reasoning behind debt consolidation is simple: move financial obligation from a high-interest account to a low-interest account. By doing this, a bigger portion of each regular monthly payment goes toward the principal rather than to the bank's earnings margin. Households frequently look for Credit Card Relief to manage increasing costs when conventional unsecured loans are too costly.

The Mathematics of Interest Reduction in the regional area

The main objective of any consolidation technique ought to be the decrease of the overall quantity of money paid over the life of the financial obligation. If a property owner in Fargo North Dakota has 50,000 dollars in charge card debt at a 25 percent rates of interest, they are paying 12,500 dollars a year simply in interest. If that exact same amount is transferred to a home equity loan at 8 percent, the yearly interest cost drops to 4,000 dollars. This develops 8,500 dollars in instant yearly savings. These funds can then be utilized to pay for the principal much faster, shortening the time it requires to reach an absolutely no balance.

There is a mental trap in this process. Moving high-interest financial obligation to a lower-interest home equity item can create an incorrect sense of financial security. When charge card balances are wiped clean, many individuals feel "debt-free" even though the debt has actually merely moved locations. Without a modification in spending routines, it prevails for customers to begin charging new purchases to their charge card while still paying off the home equity loan. This habits causes "double-debt," which can rapidly become a catastrophe for homeowners in the United States.

Picking Between HELOCs and Home Equity Loans

House owners should pick in between two primary items when accessing the worth of their residential or commercial property in the regional area. A Home Equity Loan provides a lump sum of money at a fixed rates of interest. This is often the favored option for financial obligation consolidation since it provides a predictable regular monthly payment and a set end date for the debt. Understanding precisely when the balance will be settled offers a clear roadmap for monetary recovery.

A HELOC, on the other hand, works more like a charge card with a variable interest rate. It permits the homeowner to draw funds as needed. In the 2026 market, variable rates can be dangerous. If inflation pressures return, the interest rate on a HELOC could climb, wearing down the extremely cost savings the house owner was trying to record. The introduction of Effective Credit Card Relief offers a path for those with considerable equity who choose the stability of a fixed-rate installment strategy over a revolving line of credit.

The Risk of Collateralized Financial Obligation

Moving debt from a credit card to a home equity loan alters the nature of the commitment. Credit card debt is unsecured. If a person fails to pay a credit card expense, the creditor can take legal action against for the money or damage the person's credit report, but they can not take their home without an arduous legal procedure. A home equity loan is protected by the residential or commercial property. Defaulting on this loan offers the lender the right to initiate foreclosure proceedings. Homeowners in Fargo North Dakota should be particular their earnings is stable enough to cover the new month-to-month payment before proceeding.

Lenders in 2026 generally need a homeowner to keep at least 15 percent to 20 percent equity in their home after the loan is taken out. This implies if a home is worth 400,000 dollars, the total financial obligation versus your home-- consisting of the main home loan and the brand-new equity loan-- can not surpass 320,000 to 340,000 dollars. This cushion secures both the lender and the house owner if property worths in the surrounding region take an abrupt dip.

Nonprofit Credit Therapy as a Safeguard

Before tapping into home equity, lots of economists advise an assessment with a nonprofit credit therapy company. These companies are typically approved by the Department of Justice or HUD. They supply a neutral viewpoint on whether home equity is the ideal move or if a Debt Management Program (DMP) would be more effective. A DMP includes a counselor working out with financial institutions to lower rate of interest on existing accounts without needing the homeowner to put their residential or commercial property at danger. Financial organizers suggest checking out Credit Card Relief in Fargo before financial obligations end up being uncontrollable and equity becomes the only remaining choice.

A credit therapist can also help a homeowner of Fargo North Dakota develop a reasonable budget. This budget is the foundation of any effective debt consolidation. If the underlying cause of the financial obligation-- whether it was medical costs, task loss, or overspending-- is not attended to, the brand-new loan will just provide momentary relief. For lots of, the goal is to utilize the interest savings to rebuild an emergency fund so that future expenses do not lead to more high-interest loaning.

Tax Implications in 2026

The tax treatment of home equity interest has actually changed throughout the years. Under existing guidelines in 2026, interest paid on a home equity loan or credit line is generally just tax-deductible if the funds are utilized to purchase, construct, or considerably improve the home that secures the loan. If the funds are utilized strictly for debt consolidation, the interest is typically not deductible on federal tax returns. This makes the "real" cost of the loan somewhat higher than a home mortgage, which still takes pleasure in some tax benefits for main homes. House owners ought to talk to a tax expert in the local area to understand how this affects their particular situation.

The Step-by-Step Debt Consolidation Process

The procedure of utilizing home equity starts with an appraisal. The lending institution needs a professional appraisal of the residential or commercial property in Fargo North Dakota. Next, the lending institution will examine the applicant's credit score and debt-to-income ratio. Even though the loan is protected by home, the loan provider desires to see that the house owner has the cash circulation to manage the payments. In 2026, lenders have ended up being more strict with these requirements, concentrating on long-lasting stability rather than simply the existing worth of the home.

Once the loan is approved, the funds ought to be used to settle the targeted charge card instantly. It is frequently sensible to have the loan provider pay the lenders directly to avoid the temptation of utilizing the cash for other purposes. Following the reward, the property owner ought to consider closing the accounts or, at the minimum, keeping them open with a no balance while concealing the physical cards. The goal is to ensure the credit rating recuperates as the debt-to-income ratio enhances, without the danger of running those balances back up.

Financial obligation consolidation stays a powerful tool for those who are disciplined. For a homeowner in the United States, the difference in between 25 percent interest and 8 percent interest is more than just numbers on a page. It is the distinction in between decades of monetary tension and a clear course toward retirement or other long-lasting objectives. While the threats are genuine, the potential for overall interest decrease makes home equity a primary factor to consider for anyone fighting with high-interest consumer financial obligation in 2026.

{kind=link}

Table of Contents

- – Assessing Home Equity Options in Fargo North D...

- – The Mathematics of Interest Reduction in the ...

- – Picking Between HELOCs and Home Equity Loans

- – The Risk of Collateralized Financial Obligation

- – Nonprofit Credit Therapy as a Safeguard

- – Tax Implications in 2026

- – The Step-by-Step Debt Consolidation Process

Latest Posts

Benefits of Free Credit Counseling Services in 2026

Finding Nonprofit Debt Help for 2026

Selecting Reliable Debt Settlement Services in 2026

More

Latest Posts

Benefits of Free Credit Counseling Services in 2026

Finding Nonprofit Debt Help for 2026

Selecting Reliable Debt Settlement Services in 2026